How, you might be asking, are these headline topics related to investing?

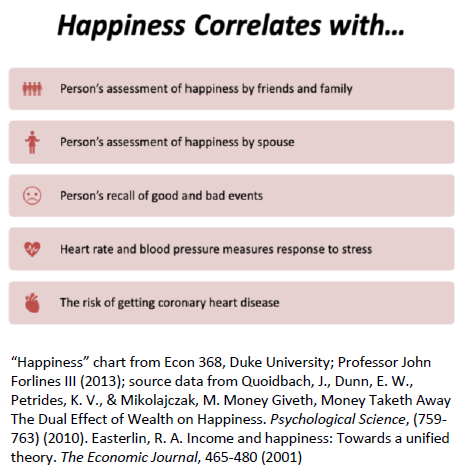

The answer, is “plenty;” they are all wrapped up in the concept of “experienced well-being,” a behavioral science (and financial) concept that at its core asks another simple question: “What is Happiness?” In my Behavioral Finance courses, in the longitudinal studies that survey tens of thousands of families over decades and in Advisor/Client interaction, the answer to this question provides a critical insight, and many researchers, students and Advisors find the answer surprising. Let’s take a look at all the research, which is summarized in the first chart. I always ask live audiences, “what is missing here?”. The answer of course is money. In institutional investment management we spend so much time dissecting markets, looking at macroeconomic trends, constructing portfolios and of course communicating with our clients, Financial Advisors. All that is necessary for proper asset allocation and risk management, our calling cards. But we also are focused on helping Advisors deal with their clients, which means we try to help them understand the emotional and psychological forces at play.

But you have to have some money to be happy, right? You do, but not nearly as much as most people think. Economists Betsey Stevenson and Justin Wolfers of the University of Michigan examined World Bank data from more than 150 countries and concluded that money will only make you a little happier, where “each doubling of your income correlated with a life satisfaction 0.5 points higher on a scale of 1 to 10.” In other words, doubling your income may make you only about 5% happier than you are right now.1

Other studies indicate that an increase in one’s income has a greater impact on happiness below a certain level. Research by Princeton University economist Angus Deaton indicates that in the U.S., $75,000 is a meaningful benchmark when it comes to money and happiness. Below that level, more money translates to a lot more happiness. Over $75,000, increases in happiness begin to level off as income continues to climb.2

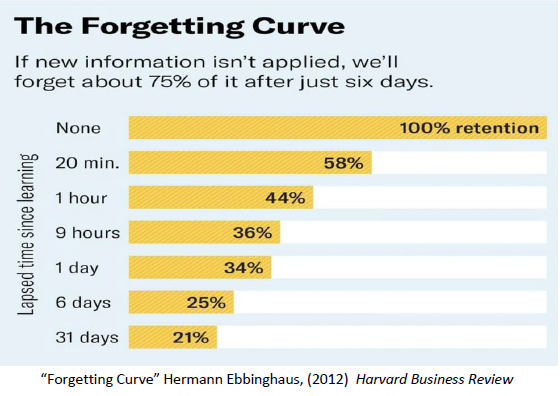

If you are an Advisor, the answer is clear: your clients are more likely to maintain a relationship with you if you’re focused on their family and their friends. The former means more opportunities for new business as families evolve; the latter means referrals. Families need truly diversified asset allocation, tax, estate and, eventually wealth planning, they don’t need to be bombarded with financial information. Staying “present” with clients also means they won’t forget you: have you contacted your clients in the last week about key life planning and family issues? If not, take a look at the “Forgetting Curve;” and remember that clients need to be refocused consistently on things they really care about family, friends, health issues.

The “Forgetting Curve” is also why we honor Veterans formally every year in November. We should care about them as part of our weekly lives as well, but we should never forget the momentous battles, wars and foreign service, that these brave Americans have fought over our history. And that’s a perfect segue to Thanksgiving, where we can celebrate being grateful—for our families, friends and freedom. According to Robert Emmons, a pioneer in the study of gratitude and a psychology professor at the University of California, Davis, gratitude involves acknowledging the good things in our lives—from the beauty of autumn leaves to the generosity of friends to the taste of a good meal—and recognizing the other people or force that made them possible.3

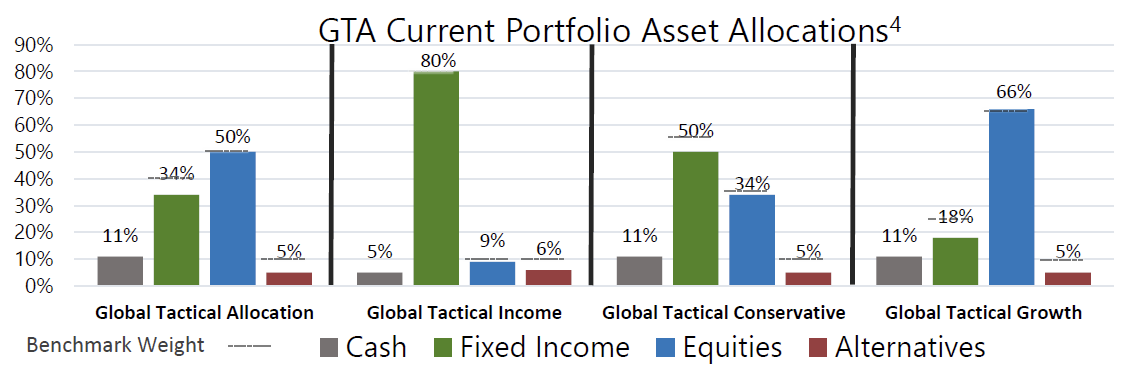

This month, we have re-positioned the portfolio while maintaining our broader asset allocation. We exited our position in global equites in favor of Europe and EM ex-Asia equities. We also initiated a position in short-term High Yield Bonds and in the US made a tactical move toward cyclical equity exposure, swapping Quality in favor of Value.

Recent Portfolio Changes

We exited our positions in broad Global equities in favor of European and Latin American equities. Easing financial conditions should re-accelerate global growth and international stocks should outperform. Accommodative global monetary policy offers support across the board, but we see the greatest opportunities in Europe and Latin America.

We initiated a position in short-term High Yield Bonds and trimmed exposure to Ultrashort Duration Bonds. In a rates up world, we prefer credit risk to duration risk. We believe that Short Term High Yield Bonds are a great value proposition in this environment.

We trimmed our position in US Quality equity and added to our position in US Value equity. We swapped some Quality for Value in our US equity book. The move increases our cyclical exposure.

Portfolio Changes

Since August 1, 2019

Cash

We initiated a position in cash. As risks persist across asset classes, and with 1-3 month treasury yields near 2%, an elevated position will help shield the portfolio from volatility.

Fixed Income (US)

We continue to be overweight in our position to Ultrashort Duration Bonds. Huge moves in interest rates have left government bonds at extremely low levels, reflecting a very bearish view of economic growth. We continue to see duration as a risk and favor short term High Yield Bonds and Ultrashort Duration at the expense of allocations to long-dated fixed income.

We maintain our position in Preferred Stocks. We maintain our conviction to the position. We expect the asset class’s attractive yield and positive tailwinds will continue to provide diversification benefits to the portfolio.

We initiated a position in short-term High Yield Bonds. In a rates up world, we prefer credit risk to duration risk. We believe that short term High Yield Bonds are a great value proposition in this environment.

Fixed Income (International)

We increased our position in Emerging Market Bonds. Given solid sovereign fundamentals and cyclical highs for yield spreads, we believe that Emerging Market Bonds provide attractive yield and portfolio diversification.

Equity (US)

We maintain positions in Quality equities. Quality equities possess pricing power, exhibit strong profitability, and have additional sustainable competitive advantages which allow businesses to remain viable over time.

We feel this holding is prudent in the later stages of the US credit cycle. We maintain a position in Value equities. We believe that Value equities provide yield at a reasonable price, are historically cheap relative to other style factors, and should outperform as the macroeconomic backdrop recovers.

Equity (International)

We maintain a position in Emerging Market equities. We believe that the most important risk to Emerging Markets (a big Chinese growth slowdown or collapse in its currency) is unlikely and US-China trade negotiations have improved on the margin. Further Chinese stimulus should boost global growth.

We initiated a position in Broad Europe and Latin American equities. We expect easing financial conditions to re-accelerate global growth and international stocks to outperform. Accommodative global monetary policy offers support across the board, but we see the greatest opportunities in Europe and Latin America.

We maintain a position in International Quality equities. We maintain our conviction to Quality factor exposure and upgraded our ex-US regional exposure.

Alternatives

We initiated a position in Broad Commodities. We expect oil and industrial metals prices will move higher as economic growth recovers. Additionally, the recent Saudi oil attack puts a risk premium into the oil price.

Please do not hesitate to contact our team with any questions. You can get more information by calling (800) 642-4276 or by emailing [email protected]. Also, visit our Contact Page to learn more about your territory coverage.

Best regards,

John A. Forlines, III

2 “$75,000” Deaton and Kahneman “High Income Improves Evaluation of Life But Not Emotional Well-Being” (2010) National Academy of Sciences

3 “Gratitude” Emmons, R. A., and Mishra, A. “Why gratitude enhances well-being: What we know, what we need to know”. In Sheldon, K., Kashdan, T., & Steger, M.F. (Eds.) Designing the future of positive psychology: Taking stock and moving forward. (2012), New York: Oxford University Press

4 Information as of 11/5/2019. Individual account allocations may differ slightly from model allocations

5 Contains international exposure

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by W.E. Donoghue & Co., LLC (W.E. Donoghue) and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities.

The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate.

The JAForlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The JAForlines Global Tactical Income Portfolio composite was created August 1, 2014. The JAForlines Global Tactical Growth Portfolio composite was created April 1, 2016. The JAForlines Global Tactical Conservative Portfolio composite was created January 1, 2018.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. Policies for valuing portfolios and calculating performance are available upon request. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects to re-investment of dividends and other earnings.

Net returns are presented net of management fees and include the reinvestment of all income. Net of fee performance was calculated using a model fee of 1% representing an applicable wrap fee. The investment management fee schedule for the composite is: Client Assets = All Assets; Annual Fee % = 1.00%. Actual investment advisory fees incurred by clients may vary.

W.E. Donoghue & Co., LLC (Donoghue) claims compliance with the Global Investment Performance Standards (GIPS®).

The Blended Benchmark Moderate is a benchmark comprised of 50% MSCI ACWI, 40% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly.

The Blended Benchmark Conservative is a benchmark comprised of 35% MSCI ACWI, 55% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly.

The Blended Benchmark Growth is a benchmark comprised of 65% MSCI ACWI, 25% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly.

The Blended Benchmark Income is a benchmark comprised of 80% Bloomberg Barclays Global Aggregate Bond Index, 10% MSCI ACWI, and 10% S&P GSCI, rebalanced monthly.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The S&P GSCI® is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800‐642‐4276 or [email protected].

W.E. Donoghue is a registered investment adviser with United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940.

{kind=link}