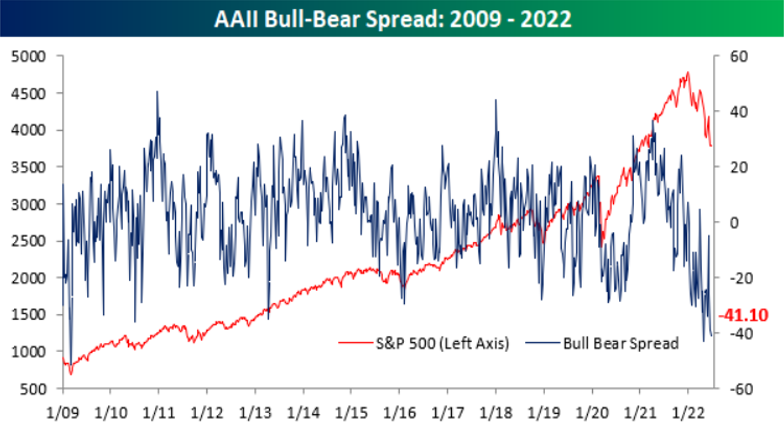

Every month, our investment committee holds a meeting to discuss the most important issues driving the macroeconomy and financial markets. This month’s meeting was especially pertinent as it comes on the heels of a substantial decline in global equities. The S&P 500 has shed over 20% from its top, officially entering a bear market. Therefore, is now a good time to buy the dip? Warren Buffett, after all, advises investors to be “fearful when others are greedy, and greedy when others are fearful”, and right now US sentiment surveys show most market participants to be scared.

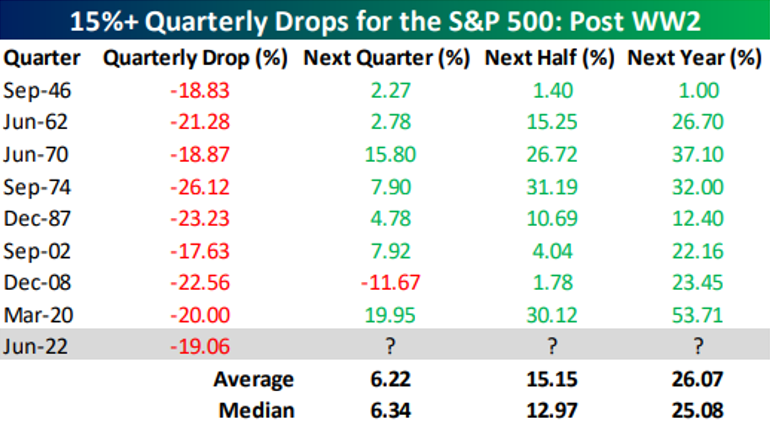

Of course, price affects sentiment and it’s been a quarter to forget for equities. As shown to the right, the S&P 500 is on pace to experience its 9th quarterly decline of 15%+ in the post-WW2 market era. Following the prior 8 quarterly drops of 15%+, the S&P averaged a gain of 6.22% the following quarter, a gain of 15.15% over the next two quarters, and a gain of 26% over the next year. Over both the next half year and year, the index was higher every single time.

However, a typical bear market drawdown for the S&P 500 is 34% and last 431 calendar days. Currently, the S&P 500 is in a 24% drawdown and 165 days since an all-time high. This would imply further downside, which our current technical analysis reiterates. The key issue that we are grappling with is whether the Fed can achieve a proverbial soft landing or whether the US and the rest of the global economy were spiraling towards recession (if it wasn’t already there).

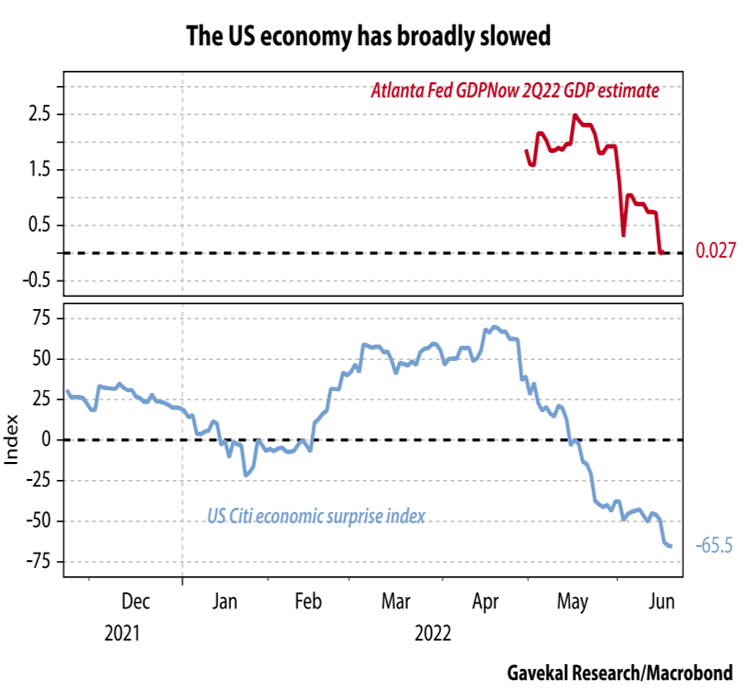

After an ugly May CPI report, Wall Street strategists are tripping over themselves to upgrade the probability of a recession. This trend is also spilling over into Main Street. Google searches for “recession” are spiking, indicating that the wider public has also become increasingly worried about an economic downturn.

Price pressures have been more persistent than initially anticipated – eating into corporate profit margins and diminishing consumers’ purchasing power. Meanwhile, the Fed is tightening monetary policy aggressively which raises borrowing costs for households and firms. Foreign economic risks stemming from geopolitical tensions in Europe and China’s struggle with Covid-19 are only adding fuel to the fire.

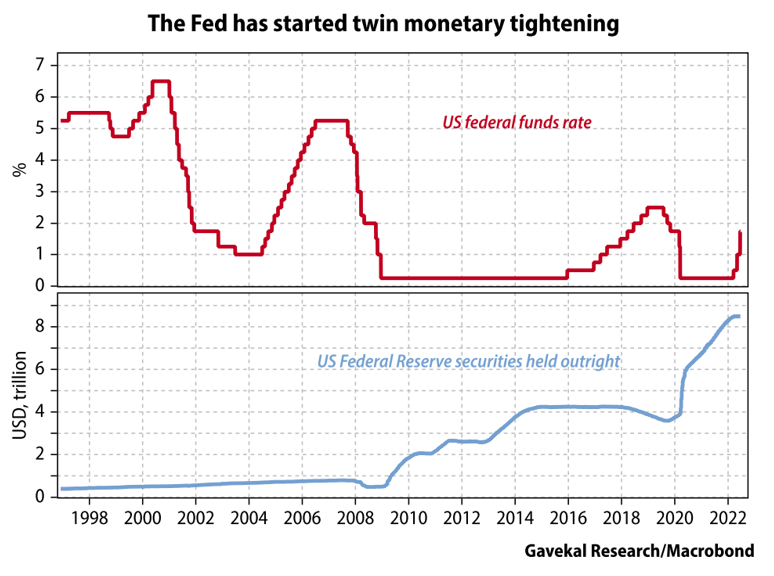

Growth has slowed broadly, and financial conditions have tightened considerably during 2022. Typically, this would elicit a response from the Fed to ease policy. The caveat this time is elevated inflation. However, we believe the Fed will eventually have to pivot to focus on the slowing growth environment or face the possibility of making another policy error. We still believe inflation will peak soon and will be the catalyst for a pivot, and we’re already starting to see signs of this in the market, with core inflation sequentially lower the past two months and now commodities rolling over. At this point, we’re not comfortable drawing conclusion to when that will happen yet. Therefore, we will refrain from adding to risk assets until more clarity emerges about the path of growth and inflation.

Our positioning this year has been defensive in our fixed income allocations and we have made moves to de-risk our portfolios. We still believe we are not in a recession, and at most a shallow one that is happening right now. However, the market is experiencing a largely unprecedented liquidity squeeze from higher rates and tighter monetary policy. It is prudent not to ignore that risk and protect portfolios against capital destroying drawdowns.

Recent Portfolio Changes

There have been no changes to the portfolio holdings since March 10, 2022.

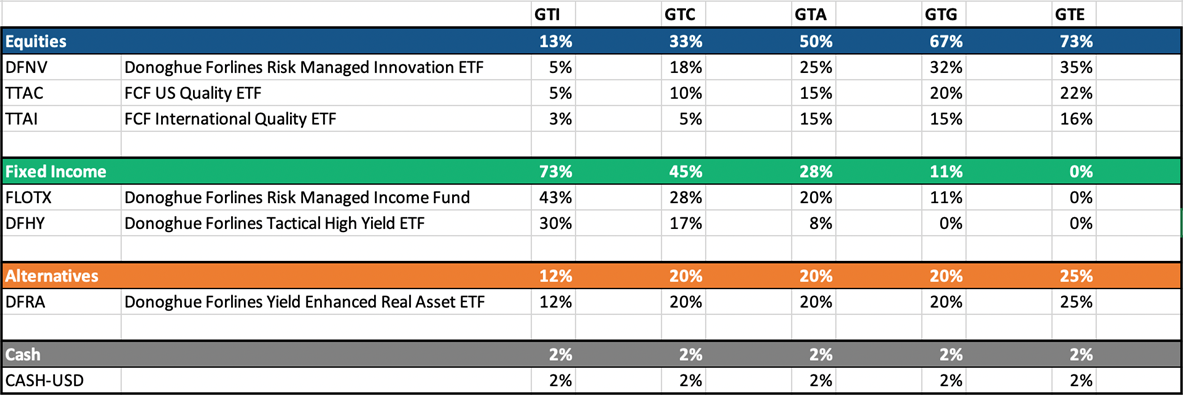

Allocations as of 03/10/2022

Holdings as of 03/10/2022

You can also get more information by calling (800) 642-4276 or by emailing [email protected].

Best regards,

Best regards, John A. Forlines III

Chief Investment Officer

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by Donoghue Forlines LLC and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities.

The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate.

The Donoghue Forlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The Donoghue Forlines Global Tactical Income Portfolio composite was created August 1, 2014. The Donoghue Forlines Global Tactical Growth Portfolio composite was created April 1, 2016. The Donoghue Forlines Global Tactical Conservative Portfolio composite was created January 1, 2018. The Donoghue Forlines Global Tactical Equity Portfolio composite was created January 1, 2018.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects the re-investment of dividends and other earnings.

Net returns are presented net of management fees and include the reinvestment of all income. Net of fee performance, when composite accounts are 100% non-fee paying, was calculated using a model fee of 1% representing an applicable wrap fee. The investment management fee schedule for the composite is: Client Assets = All Assets; Annual Fee % = 1.00%. Actual investment advisory fees incurred by clients may vary.

The Donoghue Forlines Global Tactical Allocation Benchmark is the HFRU Hedge Fund Composite. The Blended Benchmark Conservative is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% Bloomberg Barclays Global Aggregate, rebalanced monthly. The Blended Benchmark Growth is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% MSCI ACWI, rebalanced monthly. The Blended Benchmark Income is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% Bloomberg Barclays Global Aggregate, rebalanced monthly. The Blended Benchmark Equity is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% MSCI ACWI.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The HFRU Hedge Fund Composite USD Index is designed to be representative of the overall composition of the UCITS-Compliant hedge fund universe. It is comprised of all eligible hedge fund strategies; including, but not limited to equity hedge, event driven, macro, and relative value arbitrage. The underlying constituents are equally weighted. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800‐642‐4276 or [email protected].

Donoghue Forlines LLC is a registered investment adviser with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training.