2019 was a good year for risk assets and for the GT Suite. Our GTA flagship portfolio achieved high ‘teen’s performance with an average standard deviation in the single digits. That’s what risk-managed strategies are supposed to do and why we think Advisors should consider the GTA portfolio as a core complement to “free” beta models. Global Tactical Income, our multi-asset yield-focused product achieved returns in excess of nine percent with low volatility. Both of these portfolios are also available as mutual funds.

Now let’s take a look ahead; first the big picture:

The Rally in Risk Assets has Legs

World equity markets have surged over the last few months. As central banks have stepped up their easing measures, geopolitical risks have abated, and the global manufacturing slowdown appears to have stabilized. Looking ahead, there are good reasons to believe the rally will be sustained into 2020:

1) Stronger Global Growth Ahead

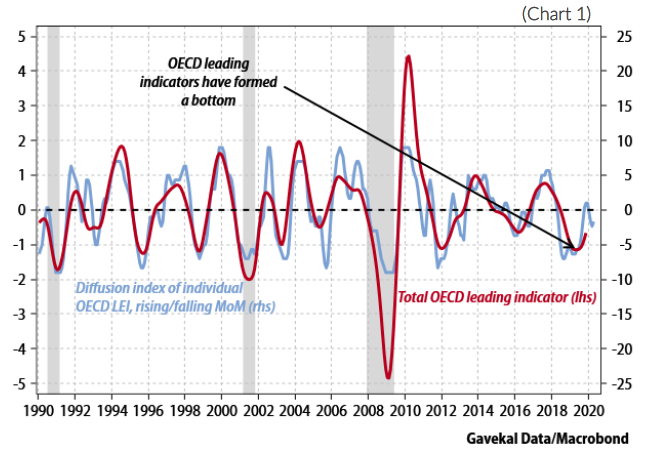

Faced with slower economic growth, a factory slump, and muted inflation expectations, the Federal Reserve and other major central banks have cut interest rates. Monetary policy affects the economy with a lag. This is one reason why the net number of central banks cutting rates has historically led global growth by about 6-9 months. The latest data on global activity has been generally supportive of our constructive thesis. Across major economies, manufacturing PMIs are off their lows and OECD leading indicators point to a rebound. (Chart 1)

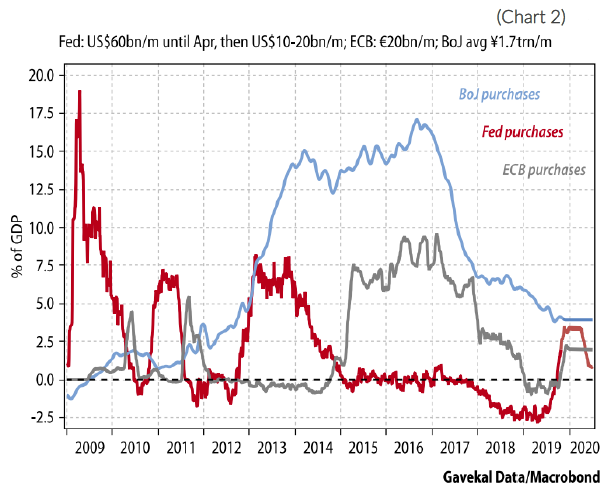

Meanwhile, for the first time since the beginning of the QE era, major central banks are printing money in concert. (Chart 2) The key economic event of the past year was the Fed shifting from quantitative tightening to balance sheet expansion. In the 15 weeks since the Fed renewed their expansionary program, the S&P 500 has not had a down week! This is extremely positive for liquidity and world markets. Fiscal settings are also expansionary across major economies. According to IMF/OECD estimates, the impulse will be mildly positive for growth in 2020.

In sum, we believe that the policy picture is favorable. Not only are central banks acting in sync, they are trending in the same direction as fiscal policy. As easier financial conditions filter through the economy, growth should edge up.

2) Large Geopolitical Risks Receding

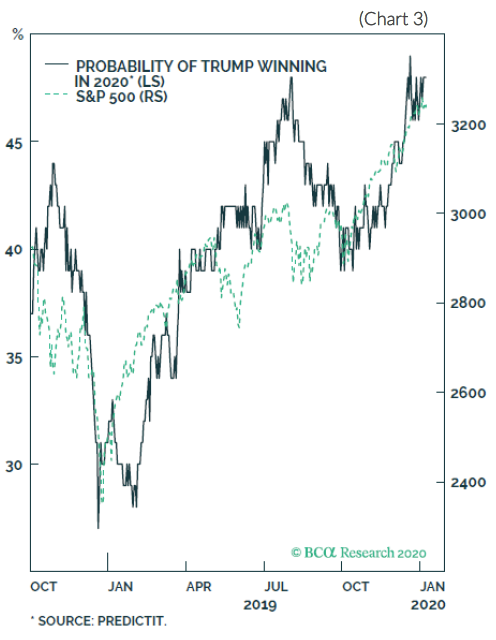

The “phase one” agreement signed earlier this month between the US and China deescalates risks and uncertainty, but strategic distrust remains. No firm schedule exists to begin “phase two” talks, but it is very likely that no negotiations will take place until after the US presidential election. And Trump has good reason to stall: partisan politics aside, the majority of voters approve of his handling of the economy. It will be his highest selling point heading into November. Any further escalation of the trade war would hurt the US economy, especially in several Midwestern states that Trump needs to carry in order to win the election. There is evidence of this in the uncanny correlation between the probability that betting markets assign to a Trump victory and the price of the S&P 500. (Chart 3) Across the pond, Brexit risks are fading, as Boris Johnson’s remarkable victory in the UK elections will give him the votes necessary to push a withdrawal bill through parliament at the end of the month.

3) We Favor Stocks, Cash & Commodities over Bonds in 2020

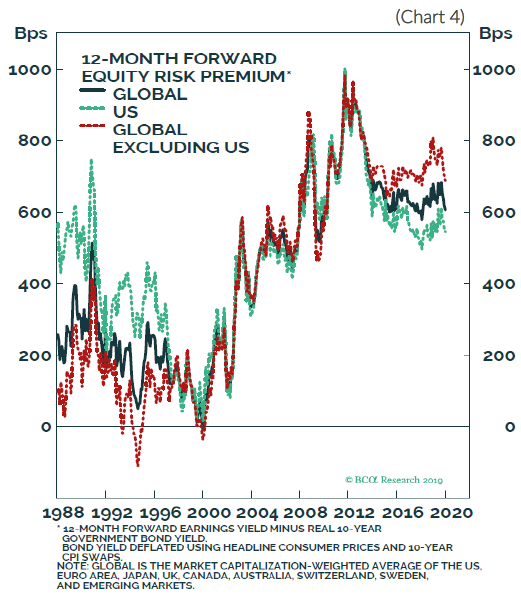

There is a very close correlation between the global manufacturing PMI and the total stock-to-bond ratio, or the degree to which stocks are outperforming bonds. It is almost always the case that when global growth picks up, equities outperform fixed income. The reason this happens is that in a stronger growth environment, corporate earnings tend to accelerate, investors become more optimistic, and P/E multiples expand. Alternatively, for bonds, faster growth generally leads to higher real bond yields, which in turn leads to lower prices. Relative valuations also favor stocks over bonds. There’s a massive gap between bond yields and equity earnings yields. We call this the equity risk premium and it remains quite high by historic standards. (Chart 4)

As global growth re-accelerates, downward pressure will be put on the US dollar. Tailwinds that have kept the dollar strong are reversing; the Fed is now printing more than its central bank peers, while trade war and Brexit risks are receding, and growth differentials no longer clearly favor the US. Commodity prices tend to closely track the dollar cycle and should outperform in a weaker dollar environment. Relative commodity valuations are also favorable and with inflation risks skewed to the upside, real assets could provide diversification.

In sum, easy monetary policy, geopolitical progress and a declining dollar all benefit growth and inflation outlooks. This is bad news for an expensive bond market and bodes well for equities and commodities.

But Time for a Breather… This is Why We Have Three Timeframes!

We are constantly looking at our GT Suite in three-time frames. (Chart 5)

Despite the optimistic view above, bullish sentiment poses near-term headwind to risk assets and stocks need to work off overbought conditions before moving higher. Net long positions in equity futures among asset managers and levered funds are now at levels that have historically preceded corrections (chart 6).

Additionally, recent market gains have relied on a handful of names. The top 5 stocks in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, and Facebook) now comprise 18% of the indexes total market capitalization, a higher share than in 2000. (Chart 7). Such weak breadth is disconcerting.

With this month’s positioning, we have modified our risk-seeking outlook over the short-term against heightened risk of a short-term correction. We reduced risk by trimming our US Value factor equity position and added a tactical hedge with a position in 7-10yr treasuries. Additionally, we added to our position in broad commodities on a pullback.

Finally, know that our Global Tactical strategies will adapt to fundamental, not emotional influences. We seek opportunities for solid risk adjusted returns and to preserve capital in risk downturns.

Recent Portfolio Changes

We trimmed our position in value equities and initiated a position in 7-10 year treasury bonds. Stocks need to work off overbought conditions before moving higher. We trimmed equity exposure from a volatile factor and added a tactical hedge with duration exposure. We do not regard this as a major realignment of our views. We will turn tactically bullish again if stocks correct from current levels.

We added to our broad commodities position. Relative commodity valuations are favorable and with inflation risks skewed to the upside, real assets could provide diversification. Stronger global growth and a weaker dollar environment should provide tailwinds.

Portfolio Changes

Since October 1, 2019

Cash

We initiated a position in cash. As risks persist across asset classes, and with 1-3 month treasury yields near 2%, an elevated position will help shield the portfolio from volatility.

Fixed Income (US)

We continue to be overweight in our position to Ultrashort Duration Bonds. We believe the long-term path for government bond yields is higher. We continue to see duration as a risk and favor short term High Yield Bonds and Ultrashort Duration at the expense of allocations to long-dated fixed income.

We maintain our position in Preferred Stocks. We maintain our conviction to the position. We expect the asset class’s attractive yield and positive tailwinds will continue to provide diversification benefits to the portfolio.

We initiated a position in short-term High Yield Bonds. In a rates up world, we prefer credit risk to duration risk. We believe that short term High Yield Bonds are a great value proposition in this environment.

We initiated a position in 7-10 year Treasuries. Stocks need to work off overbought conditions before moving higher. We believe 7-10 year treasuries will provide a ballast for the portfolio as a tactical hedge.

Fixed Income (International)

We increased our position in Emerging Market Bonds. Given solid sovereign fundamentals and cyclical highs for yield spreads, we believe that Emerging Market Bonds provide attractive yield and portfolio diversification.

We initiated a position in Emerging Market Local Currency Bonds. As global growth recovers, the dollar should weaken. Emerging market local currency bonds provide an excellent dollar hedge and deliver attractive yields.

Equity (US)

We maintain positions in Quality equities. Quality equities possess pricing power, exhibit strong profitability, and have additional sustainable competitive advantages which allow businesses to remain viable over time. We feel this holding is prudent in the later stages of the US credit cycle.

We initiated a position in Value equities. We believe that Value equities provide yield at a reasonable price, are historically cheap relative to other style factors, and should outperform as the macroeconomic backdrop recovers.

Equity (International)

We maintain a position in Emerging Market equities. We believe that the most important risk to Emerging Markets (a big Chinese growth slowdown or collapse in its currency) is unlikely and US-China trade negotiations have improved on the margin. Further Chinese stimulus should boost global growth.

We initiated a position in Broad European equities. We expect easing financial conditions to re-accelerate global growth and international stocks to outperform. Accommodative global monetary policy offers support across the board, but we see the greatest opportunities in Europe.

We initiated a position in International Quality equities. We maintain our conviction to Quality factor exposure and upgraded our ex-US regional exposure.

Alternatives

We initiated a position in Broad Commodities. We expect oil and industrial metals prices will move higher as economic growth recovers. Relative commodity valuations are favorable and with inflation risks skewed to the upside, real assets could provide diversification.

Please do not hesitate to contact our team with any questions. You can get more information by calling (800) 642-4276 or by emailing [email protected]. Also, visit our Contact Page to learn more about your territory coverage.

Best regards,

John A. Forlines, III

1 Information as of 1/15/2020. Individual account allocations may differ slightly from model allocations

2 Contains international exposure

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by W.E. Donoghue & Co., LLC (W.E. Donoghue) and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities.

The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate.

The JAForlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The JAForlines Global Tactical Income Portfolio composite was created August 1, 2014. The JAForlines Global Tactical Growth Portfolio composite was created April 1, 2016. The JAForlines Global Tactical Conservative Portfolio composite was created January 1, 2018.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. Policies for valuing portfolios and calculating performance are available upon request. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects to re-investment of dividends and other earnings.

Net returns are presented net of management fees and include the reinvestment of all income. Net of fee performance was calculated using a model fee of 1% representing an applicable wrap fee. The investment management fee schedule for the composite is: Client Assets = All Assets; Annual Fee % = 1.00%. Actual investment advisory fees incurred by clients may vary.

W.E. Donoghue & Co., LLC (Donoghue) claims compliance with the Global Investment Performance Standards (GIPS®).

The Blended Benchmark Moderate is a benchmark comprised of 50% MSCI ACWI, 40% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly. The Blended Benchmark Conservative is a benchmark comprised of 35% MSCI ACWI, 55% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly. The Blended Benchmark Growth is a benchmark comprised of 65% MSCI ACWI, 25% Bloomberg Barclays Global Aggregate, and 10% S&P GSCI, rebalanced monthly. The Blended Benchmark Income is a benchmark comprised of 80% Bloomberg Barclays Global Aggregate Bond Index, 10% MSCI ACWI, and 10% S&P GSCI, rebalanced monthly.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The S&P GSCI® is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800‐642‐4276 or [email protected].

W.E. Donoghue is a registered investment adviser with United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940.