From Pain to Gain

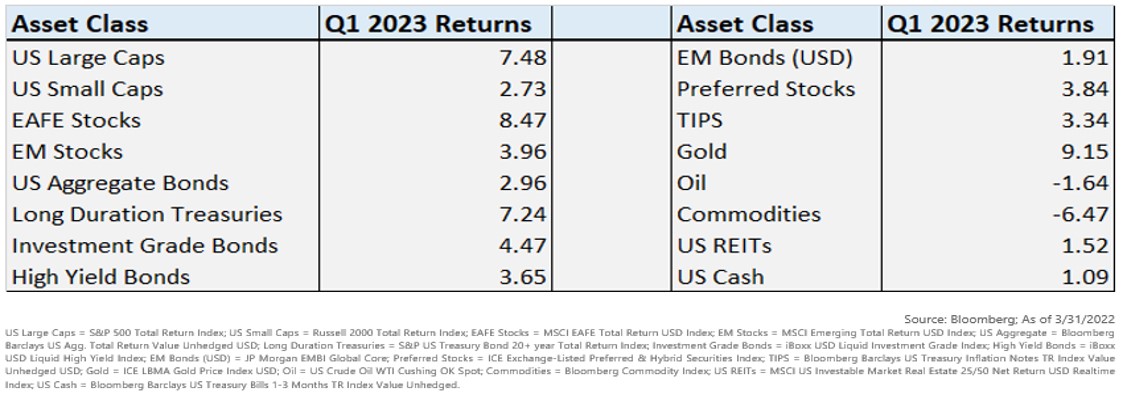

Asset prices fluctuated considerably during the beginning of 2023 but ended up posting widespread gains. A decline in U.S. Treasury yields helped boost both fixed income and equity returns, while commodity prices fell.

Financial markets digested multiple crosscurrents during the first quarter, including stress in the global banking system, falling inflationary pressure, and mixed global growth data.

Source: Bloomberg As of 3/31/2022

Banking Crisis?

The wounds of the 2008 financial crisis cut deep. So unsurprisingly when another US bank fails, everyone sits up and takes notice. This past quarter, Silicon Valley Bank collapsed (2nd largest failure in history), creating a deposit crisis among other regional banks, and sending shockwaves through the entire industry. Subsequently, Signature Bank and First Republic Bank failed as well.

The FDIC, Treasury, and Federal Reserve announced a large federal response to back customer deposits and provide liquidity to stave off systemic risk.

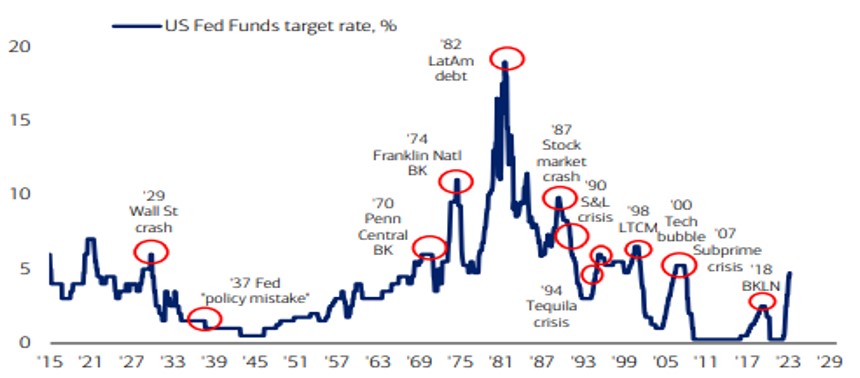

The question for investors is whether this was a one-off triggered by problems unique to these banks, or whether it was a sign of broader weaknesses in the US banking sector. We believe both are true… while these banks failed because of bank specific dynamics, the Fed’s aggressive rate hike policy revealed their weakness and perhaps this is just the first crack to an already unstable economy. We need to remember a year ago Fed funds was 0% and the yield curve 40bps steep; today Fed funds rate is 4.75% and yield curve is deeply inverted. An inverted yield curve disrupts the whole bank business model of borrowing short to lend long.

U.S. Fed Funds Target Rate %

Source: BofA Global Investment Strategy, Bloomberg Global Financial Data

The good news is the situation is very different than 2008. The concern is not so much that banks are holding on to a lot of mispriced assets, but that they can no longer fund themselves with higher rates and an inverted yield curve, and thus do not have much of a business model.

Therefore, this crisis seems to be weeding out where the most excess was built during an era of low cost of capital. For example, SVB delivered remarkable returns by embracing an aggressive growth strategy, at a time, and a place, when such a strategy was rewarded—until it was not.

In the meantime, most US banks will face more regulation, additional government scrutiny, reduced animal spirits and a diminished appetite to lend. This likely means weaker economic growth. A powerful solution to this problem would be for the Fed to cut rates, but will they pivot from their ongoing battle with Inflation?

Monetary Policy is Tight

If you did not think so before, it is clear now how tight monetary policy is as it filters its way through financial conditions and the entire economic system. It is often said that when the Federal Reserve starts to raise interest rates, it generally keeps doing so until something breaks. Well, something just broke. So, has the Fed now caused enough damage to take a step back?

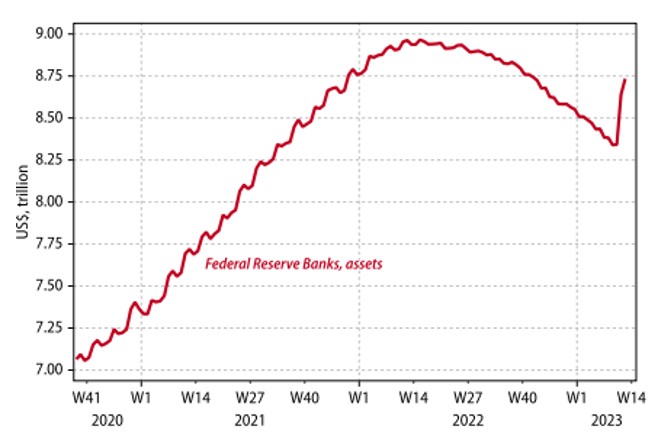

Let us first look at what the Fed is doing. As the pain grew, the Fed rapidly returned to being a provider of excess liquidity, wiping out 60% of the quantitative tightening program over the last year.

Gavekal Research/Macrobond

Now let us look at what the Fed is saying. Powell created a clear ground for changing the trajectory of policy conditional on broader pain in the banking sector hitting the real economy. Therefore, if that does not emerge and the strong inflation and labor market data holds up then rate hikes could re-accelerate.

The juxtaposition of interest rate policy and financial stress poses risks of monetary overkill. However, the Fed will want to tread lightly to maintain credibility. We believe that they overreacted to the inflation slump during the Covid crisis by easing financial conditions too far for too long. The eventual result was an overheating economy and overly hot inflation. The risk now is that the Fed is tightening conditions so much that it has initiated a disinflationary process that will overshoot to the downside, and may in turn, cause a recession.

Weaker Growth Ahead

At this stage, anyone playing “recession bingo” at home would stand up and yell “bingo”. After all, we now have an inverted yield curve, falling leading indicators, ISM surveys below 50 (ISM manufacturing survey is a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms. Any score below 50 represents a contraction in business activity), rising defaults on auto loans, and weaker real estate markets across the US.

And when banks fail, it is hard to feel super confident about the trajectory of the economy, even if these are “bumps in the road” and not signs of banking system collapse. As a result, unless the Fed’s policymakers want to end up making another policy mistake (rates too low for too long following Covid), they are likely to press pause on rate hikes and quantitative tightening. If the Fed does pivot, this episode might have seen an accelerated bottom for this cycle. If the Fed pushes back, and reaccelerates rate hikes, the market will see more pain.

Long-Term: Structural Inflationary Pressures to Persist.

While disinflation will capture headlines this year, we believe secular inflation will be an investment theme for the next decade. Structural shifts in the global economy from Covid, other geopolitical events, and demographics point to the end of the deflationary era that’s dominated markets over the last two decades. A “second surge” of inflation akin to the 1970s is still a large risk and this bout has closely tracked that path thus far.

Therefore, old ways of diversifying don’t work as well today. Structural macro reversals have spelled the end of 60/40 and turned stock/bond correlations positive, in line with 20th century averages.

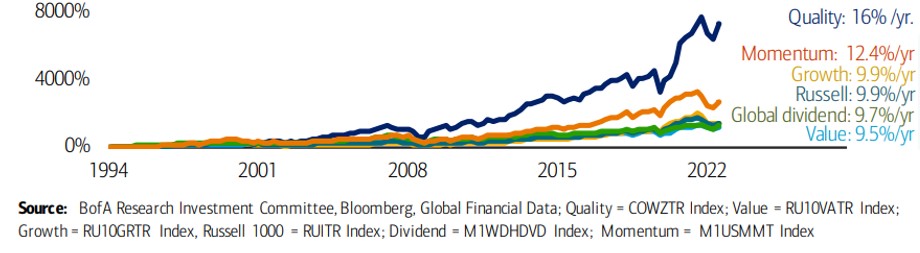

A Flight to “Quality” Equities

Quality as a factor can be defined in a number of ways. We believe free cash flow is the best expression and is a staple of our portfolios. Quality is uncorrelated to other factors and outperforms in late cycle/recessionary environments. In fact, it outperforms in a number of environments and on a risk adjusted basis. We believe high quality stocks are likely to lead the next bull market and through the next decade of investing.

Asset Market Implications

Asset Markets remain at a critical juncture. Stocks have been rangebound for a year now, but still well off their previous highs. Bond yields have started to come down for the first time in years and the yield curve is deeply inverted. Economic data, specifically inflation, will be extremely important in dictating future Fed policy. We do believe we are at the beginning of a cyclical disinflationary cycle and the Fed will have to eventually pivot. While that indicates we are closer to a firm equity market bottom and new bull market, ultimately, we believe there will need to be more pain in the economy and markets before that happens. The technical picture for stocks has improved in recent months, but we remain cautious to elevated volatility.

We also expect volatility to increase, and with it, the importance of tactical asset allocation in 2023. We look forward to helping clients navigate this environment!

Donoghue Forlines Portfolios

In today’s environment, the 60/40 retirement rule is stuck in the past. Advisors are challenged to rethink foundational portfolio elements of investor portfolios – which means seeking out strategies that bolster the “core” going forward. With no cheap assets, tactical and unconstrained management is now more important than ever.

We continue to focus on the need to help craft easy-to-understand, longer-term narratives for Advisors and their Clients. Panicking and abandoning diversified investment strategies during volatility and market crashes/surges is a time-tested losing proposition.

Donoghue Forlines solutions are designed to be client-centric and deliver strong risk-adjusted return streams through both our rules-based, tactical strategies as well as our global macro, fundamentally driven tactical solutions. We aim to capture the majority of the upside but more importantly to avoid the majority of the downside.

We have continued to carefully assess exposure across all our portfolios over the past quarter, as per our risk management process. Our positioning is outlined in more depth below. We have made moves to protect against downside in current markets.

We will stay vigilant with our goal of seeking strong risk-adjusted returns. Please visit our website at www.donoghueforlines.com for our latest information including Fact Sheets for the entire suite of products. We will stay vigilant with our goal of seeking strong risk-adjusted returns. Thank you for your confidence in Donoghue Forlines. Please let us know if you have any questions.

Best regards,

Best regards,

Jeffrey R. Thompson

Chief Executive Officer

Portfolio Manager

The following reflects Donoghue Forlines’ portfolios positioning as of March 31, 2023.

Donoghue Forlines Dividend Portfolio

Positioning: 50% allocated to large and mid-sized high yielding stocks with a diversified sector exposure and quality orientation. 50% exposure to short-term treasuries.

During the quarter, we received one tactical signal. On March 24th, we sold 50% exposure to large and mid-sized high yielding stocks and allocated 50%to short term treasuries. On March 6th, the portfolio was reconstituted and rebalanced.

Donoghue Forlines Momentum Portfolio

Positioning: 100% allocated to large and mid-sized stocks exhibiting strong short-term momentum with diversified sector exposure and quality orientation.

During the quarter, there were no technical overlay signals. On March 6th, the portfolio was reconstituted and rebalanced.

Donoghue Forlines Treasury Portfolio

Positioning: 100% invested in intermediate-term U.S. Treasury bonds via ETF exposure.

During the quarter, the portfolio did not receive a technical trigger and remained 100% invested in intermediate-term U.S. Treasury bonds.

Blended Solutions

The blended solutions combine the best ideas from our rules-based and global macro solutions into long-term investment solutions.

Donoghue Forlines Income Portfolio

The DF Income Portfolio’s asset allocation at the quarter end is as follows: 62% in cash, 29% in fixed income, 5% in equities, and 4% in alternatives.

Target Allocations: *(50%) in Donoghue Forlines Tactical Income Fund; (36%) in Donoghue Forlines Risk Managed Allocation Fund; (12%) in Donoghue Forlines Tactical High Yield ETF; and 2% Cash.

Donoghue Forlines Dividend & Yield Portfolio

The DF Dividend and Yield Portfolio’s allocations at quarter end are as follows: 46% in cash, 21% in fixed income, 25% in equities, 8% in alternatives.

Target Allocations: Donoghue Forlines Tactical Income Fund (49%); Donoghue Forlines Tactical Allocation Fund (19%); Donoghue Forlines Risk Managed Income Fund (15%); Donoghue Forlines Dividend Fund (12%); Donoghue Forlines Momentum Fund (3%); and 2% Cash.

Donoghue Forlines Growth & Income Portfolio

The DF Growth and Income Portfolio’s allocations at quarter end are as follows: 27% in cash, 23% in fixed income, 41% in equities, and 9% in alternatives.

Target Allocations: Donoghue Forlines Tactical Allocation Fund (38%); Donoghue Forlines Momentum Fund (20%); Donoghue Forlines Risk Managed Income Fund (5%); Donoghue Forlines Tactical Income Fund (20%); Donoghue Forlines Dividend Fund (15%); and 2% Cash.

IMPORTANT RISK INFORMATION

The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors, or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate.

Past performance is no guarantee of future results. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. Returns can vary dramatically in separately managed accounts as such factors as point of entry, style range and varying execution costs at different broker/dealers can play a role. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations to purchase or sell such securities. Forecasts are inherently limited and should not be relied upon as an indicator of future results. There is no guarantee that these investment strategies will work under all market conditions, and each advisor should evaluate their ability to invest client funds for the long-term, especially during periods of downturn in the market. Some products/services may not be offered at certain broker/dealer firms.

The investment descriptions and other information contained in this Market Commentary are based on data calculated by Donoghue Forlines LLC (Donoghue Forlines) and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. This report should be read in conjunction with Donoghue Forlines’ Form ADV Part 2A and Client Service Agreement, all of which should be requested and carefully reviewed prior to investing.

There can be no assurance that the purchase of the securities in this portfolio will be profitable, either individually or in the aggregate, or that such purchases will be more profitable than alternative investments. Investment in any Portfolio, or any other investment or investment strategy involves risk, including the loss of principal; and there is no guarantee that investment in Donoghue Forlines’ Portfolios or any other investment strategy will be profitable for a client’s or prospective client’s portfolio. Investments in Donoghue Forlines’ Portfolios, or any other investment or investment strategy, are not deposits of a bank, savings, and loan or credit union; are not issued by, guaranteed by, or obligations of a bank, savings, and loan, or credit union; and are not insured or guaranteed by the FDIC, SIPC, NCUSIF or any other agency. The composite strategy provides diversified exposure to various asset classes such as equities, fixed income, and alternatives utilizing liquid exchange-traded products. Diversification does not guarantee a profit or protect against a loss.

Donoghue Forlines LLC is a registered investment adviser with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training.